Monthly Download | Construction Update | February 2017

Adding 20 million square feet in 2016, the Philadelphia industrial market ended the year with nearly 1.1 billion square feet of inventory. To bring this market into focus, Lee & Associates of Eastern Pennsylvania (LAEP) focuses on our Core Data Set (CDS) -- specifically buildings 100,000 SF and greater. We also apply this criteria when tracking development and construction activity across the market.

In 2016, Central Pennsylvania and the Lehigh Valley accounted for over half of the new construction activity, adding 5 million square feet and 6.8 million square feet, respectively. Southern New Jersey, emerging as the Philadelphia market’s third largest driver of construction activity, contributed 4.7 million square feet of new construction. More established submarkets, such as the I-81 Corridor and Suburban Philadelphia, also contributed new inventory, but not at the rate of their market-leading neighbors, a trend we expect will continue in 2017.

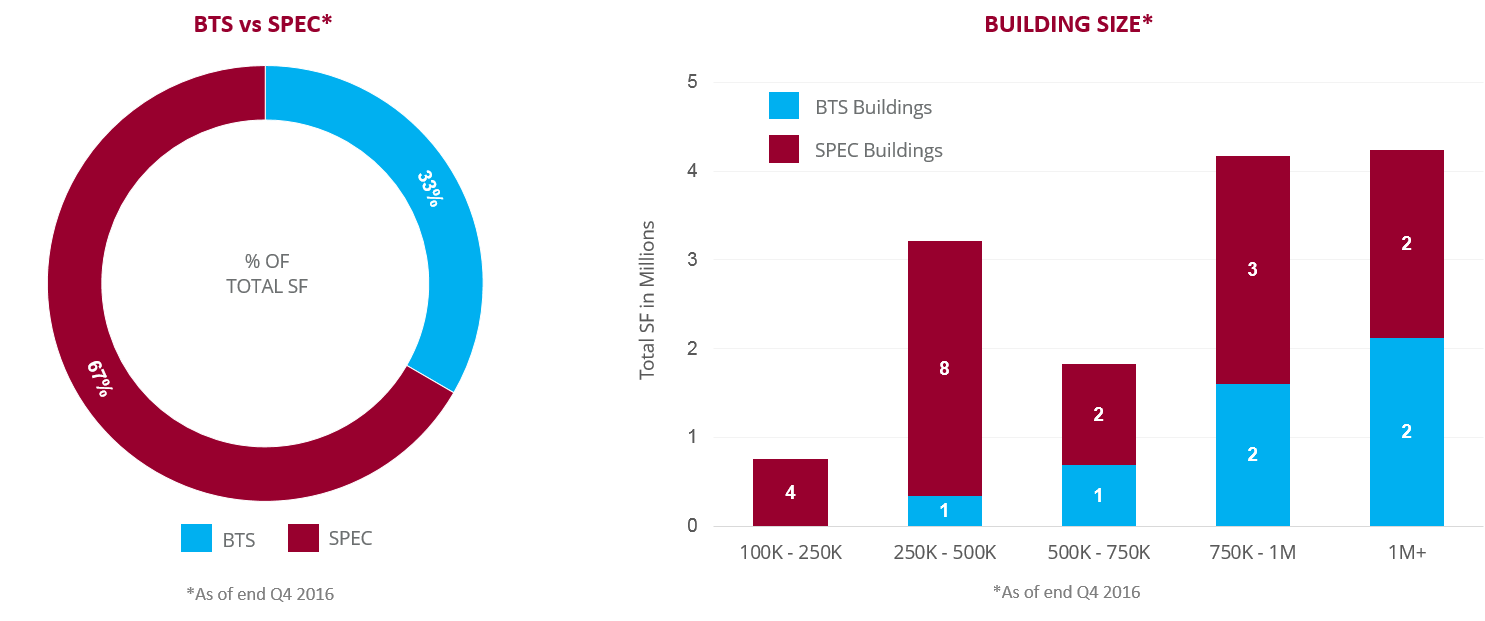

Construction activity was dominated by speculative development in 2016, accounting for 80% of all delivered space in our Core Data Set. In Central Pennsylvania, 100% of the deliveries were speculative construction; in the Lehigh Valley speculative deliveries accounted for 76% of all new inventory. Demand remained strong with only 56% of the delivered speculative space in Central PA available for lease by the end of 2016. That figure was even lower in the Lehigh Valley and Southern New Jersey, where only 28% and 20% of delivered speculative space remained available for lease. Only a few weeks into 2017, another one million square feet of the available speculative space delivered in 2016 has already been leased in the Lehigh Valley and Southern New Jersey.

Of the 14 million square feet of space still under construction at the end of Q4 2016, 67% was speculative. In Q1 2017, 2.5 million square feet of that speculative space has been delivered across Central PA, the Lehigh Valley, and the I-81 Corridor. As a result, less than 60% of the remaining 11.8 million square feet of construction activity across the market is speculative. The Lehigh Valley is leading the market with 4.3 million square feet of overall construction activity, while the Central PA, Southern New Jersey, and the I-81 Corridor markets are experiencing 2 to 3 million square feet each. The Lehigh Valley and the I-81 Corridor continue to drive speculative construction activity, representing 80% and 70% of each market’s respective overall activity as we begin 2017.

Taking a closer look at the design specifications across the market, the majority of projects (76%) were designed at 36 feet clear height or more. A significant majority (88%) are cross-dock projects. While sizing demands are relatively unique to a specific user or potential occupier, about 46% of current speculative projects have footprints 250,000 to 500,000 square feet. 31% have footprints 750,000 square feet or more. When including BTS projects; 58% are 500,000 square feet or greater, 42% are 750,000 square feet or more, and 21% are 1 million square feet or more.

As we move into 2017, fully entitled sites are becoming increasingly scarce, driving land prices higher throughout the region. There is currently 40 million square feet across the market that is either approved or is being prepped to be construction-ready. With a healthy pipeline in place, construction activity should continue on par with 2016. However, if demand remains as strong as it was last year, markets like the Lehigh Valley and Southern New Jersey may struggle to keep pace.

__

Any questions regarding the Eastern Pennsylvania market please contact us at 717.695.3840 or 610.400.0499.